A version of this essay was published at https://www.firstpost.com/opinion/shadow-warrior-svb-collapse-how-system-wide-problem-created-by-fed-led-to-us-second-largest-bank-failure-12307942.html

There are several interesting questions about the spectacular and sudden collapse of the Silicon Valley Bank (SVB). Once you get over the initial shock of this possibility in this day and age (bank runs were only supposed to happen in the bad old days), then you will be confronted with the question of what it means not only for US banks, but also for your investment strategy going forward.

In a sense, the tension between economists and finance people, who may not think alike all the time, is coming to the fore in awkward ways. Finance professionals try to avoid risk for their companies. Economists try to manage the economy according to their orthodoxies.

What is of interest is not only how rapidly the collapse happened, but also why. Plus, what the bailout (it sure smells like one, although the US authorities are emphatic that what they are doing is not a bailout) means in terms of moral hazard, and the possibility of further contagion that could lead to systemic collapse. And finally, where the safe havens are, if any, especially in view of the possible loss of primacy for the US dollar.

The apparent bare facts are as follows: there was an old-fashioned bank run on SVB, as spooked depositors withdrew about $42 billion in one day, out of roughly $219 billion total deposits taken in. In order to make the payouts, SVB had to liquidate long-term bonds that it held. These bonds, both in US Treasuries and in fixed-rate mortgage-backed securities, had lost value because of the steady increase in interest rates by the US Federal Reserve. The forced selling of these bonds caused SVB to become cash-negative (they had negative $958 million in cash). An attempt to raise more funds failed. The US government put it into receivership.

The proximate cause of the collapse is two-fold: the bank run, which was accelerated enormously because of the fact that it could be done electronically, rather than by people showing up at the doors to the bank and trying to withdraw their cash physically. Besides, SVB’s depositors were overwhelmingly large players, most of whom had balances greater than the $250,000 for which accounts are normally insured.

Once these large players, often VC-backed companies or VCs themselves, got a whiff of trouble, they were quick to act. Besides, the surprising readiness of the US government to bail them out by promising to cover all deposits, not just those below $250,000, suggests they are influential.

The preponderant cause, however, lies in a poor decision made by the SVB. As all banks do, they had to park the deposits they took in somewhere where they could get a return. Unfortunately for them (in hindsight) they chose to invest in long-term bonds. At the time (before covid) it was probably not a bad idea, because if held to maturity these bonds would yield a modest return, and they are backed by the US government.

Unfortunately, what happened is that when they bought the bonds, interest rates were at a low, and so the return on these bonds was acceptable. But then the Federal reserve started hiking up the interest rates rapidly, for good reason: to control inflation. That made the yield on the bonds go up, and conversely the bonds lost value. Especially if you had to sell them they caused you to immediately take a big ‘haircut’ as you had to write your assets down and take the loss. This is a system-wide problem, and SVB was an extreme case (but not the only one).

Which brings us to the root cause. That is the Covid-19 or Wuhan virus epidemic. One of the ways in which the US government, and other Western governments, tackled the economic fallout from shutdowns and loss of business activity was to try to stimulate the economy by basically printing a lot of money, and giving it to the public. There was debate at the time about whether this was a good idea, but everyone seems to have got behind that plan.

On the face of it, when there were lots of business failures due to the lockdowns and other disruptions, and job losses, it seemed fair to just give people a lot of money to tide them over, and to stimulate the economy. Besides, the ‘Universal Basic Income’ idea was hot among prominent economists at the time. It was considered fair that everybody would have a small but adequate income doled out by the State: a sort of Welfare State on steroids.

Every US taxpayer received a few thousand dollars as a ‘gift’, which they probably used for emergency expenditures or saved. Interestingly, the Indian government did not give out a dole; instead, it tried to fend off the hunger problem by giving out free grains and pulses to large numbers of people. In other ways, too, India took a relatively cautious approach, and did not stimulate the economy a lot during the pandemic. This proved wise.

It appears now that the vast amounts of money thus printed in the West were inflationary (not surprisingly). In the case of the US, ever since Richard Nixon delinked the dollar from gold, it has been possible for the government to print any amount of money.

On top of this, the Ukraine war caused hydrocarbon prices to surge worldwide, as well as food prices, for a variety of reasons, including sanctions on Russia on its oil and gas, and the sudden disappearance of both Russian and Ukrainian products such as fertilizer.

Inflation shot up from about 0-1% to about 6%, which is uncomfortable, and pinches the man on the street. Unfortunately, just about the only way to deal with this situation (short of ending the war in Ukraine and related disruptions, which is politically uncomfortable) is the blunt instrument of interest rate increases from the US Federal Reserve.

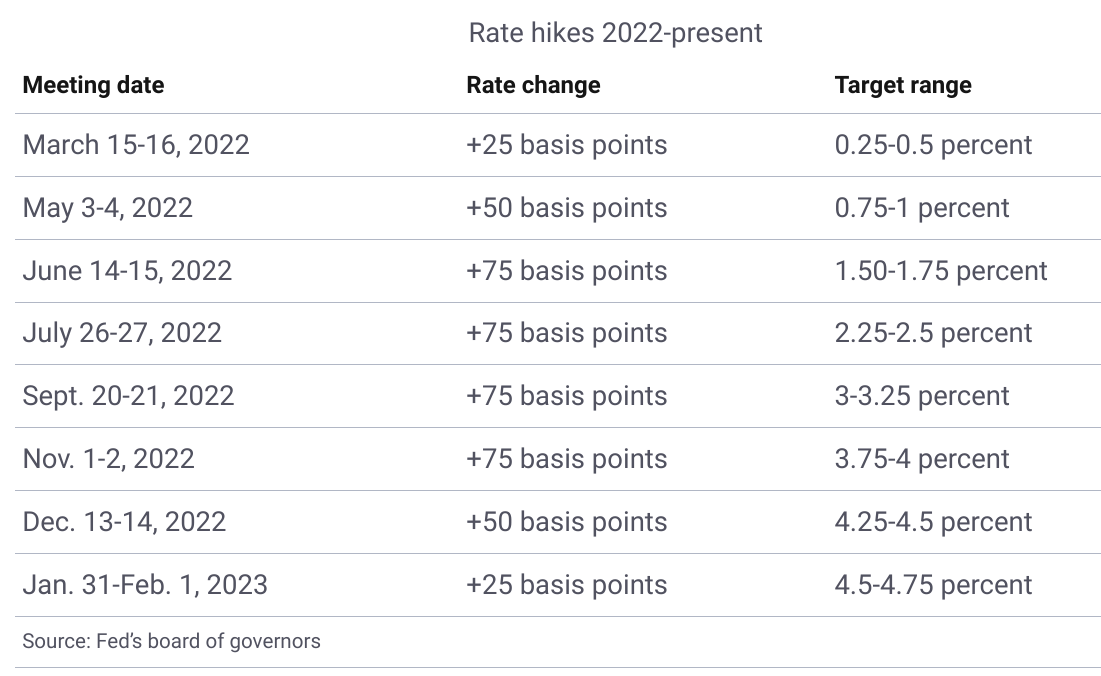

The US Federal funds rate, which had hovered around 0-0.25% between March 2020 and March 2022 went up in several increments of 0.75%, so that they are now at around 4.75%.

The Fed has, most recently, slowed its pace of interest rate increases, and the latest, on February 1 was only 0.25%. But the damage to banks was already done, as in the following post by Balaji Subramanian, a venture capitalist and crypto investor (note that).

Inflation is a tax on savers, and a boon for borrowers. Some economists (for example Abhijit Banerjee) have suggested that governments (the biggest borrowers) may use it as an “inflation tax” to degrade their debt obligations, although there is no evidence that this was the case here.

This suggests systemic risk, though, and sure enough, two other banks, Signature and Silvergate, also collapsed. Silicon Valley Bank was the second biggest bank in US history to collapse; Signature was the third biggest. Now there may be other factors as well: for example Silvergate was a crypto-focused bank, and Signature had exposure to crypto, and after the FTX fiasco a few weeks ago, that segment is under pressure.

When Silicon Valley Bank went into a tailspin, one of the biggest voices arguing for its rescue (note: he claims it is not a bailout) was Bill Ackman, a billionaire hedge fund manager. Ackman may or may not be correct, but what is surely interesting to Indian observers is that he was quick to denounce the Adani group and give a certificate of authenticity to Hindenburg. Twitter user @thehawkeyex pointed this out, and how the CFO of Adani mocked Ackman. Karma, I suppose. Adani is still standing, but FTX, and now SVB, are history.

Having said all this, the US has a way of being able to deal with financial firestorms, such as the global financial crisis of 2007-08. There is also the TINA factor. Where else would you put your money? Chinese yuan? Not likely! Euro? Isn’t Europe in a tailspin?

But there are a couple of ominous things in the background. Ever since Bretton Woods just after WW2, the US dollar has been the reserve currency for international transactions, in particular for oil and gas. Now, especially after sanctions on Russia, there are attempts to create non-dollar blocs. For instance there are rouble-rupee trades, and the yuan is increasingly used by China for its trade.

More importantly, there was a recent Saudi-Iran agreement brokered by China. This is startling, because Saudi Arabia has been firmly in the American camp, and Iran has been firmly out of it. These two oil giants being shepherded by China is remarkable, and it may signal that Saudi Arabia may now be looking at the petro-yuan in addition to the petro-dollar.

This is a danger to the value of the US dollar, demand for which has continued to be high because of its central role in trade and contracts between third parties, despite the loss of its earlier predominance due to America’s trade surplus in manufactured goods. If more and more contracts are denominated in other currencies, it may lose its de facto reserve currency position.

From an individual point of view, that raises questions. Where should one park one’s assets? The traditional answer has been the stable US dollar. Is that still the right answer? Should one look at commodities (notoriously volatile), or real estate (not very liquid), or gold (physical gold is not very easy to handle)?

I am tempted to say that in these volatile times, the traditional wisdom of the Indian woman may be the right approach: buy gold. And not paper gold, because that is dependent on how much you trust the intermediary that’s giving you their assurance that they will give you back your gold intact.

Things will take some time to settle. It is likely that the contagion will hit a few more American banks. I hope that it can be contained, and there will not be the global financial collapse that some doomsters have been predicting for a while. But Silicon Valley Bank is definitely the canary in the coalmine, pointing to major underlying issues.

1680 words, 15 Mar 2023

Share this post